Green Banking for Environmental Management: A Paradigm Shift

Kanak Tara1 * , Saumya Singh1 and Ritesh Kumar2

1

Department of Management Studies,

ISM,

Dhanbad,

826004

India

2

CSIR-Central Institute of Mining and Fuel Research,

Dhanbad,

826015

India

http://dx.doi.org/10.12944/CWE.10.3.36

The present era of industrialization and globalization has added a lot of comfort and luxury to human life but has also lead to an alarming situation of huge environmental degradation incorporated with all the involved activities. Today, the entire sector in the world economy is facing huge challenge to deal with the environmental problems and their related impacts in their day to day businesses. Not only the business firms have realized the importance of the environment but more than that an immense awareness is seen among the consumers and general public for the same. Due to all these reasons the business organizations have started modifying their activities and strategies so as to ensure protection to our natural resources and environment. In this context the financial sector and especially the banks can play an important role in promoting environmental sustainability. Sustainability is one of the most important factors driving the strategy making process of the business fraternity. Though we have realized very late that any development needs to be sustainable and equitable but the positivity lies in the fact that currently there has been an increasing concern for sustainable development among all the sectors in the economy including the financial sector. In financial sector, the various services that have adopted green business are banks, stock brokerage companies, credit card companies and also the companies of consumer finance. The concern for environmental sustainability has given mass recognition to the concept of corporate social responsibility. The potential benefits of the concept has gained the interest of the regulatory authorities, society, NGOs, employees, customers as well as the international bodies to the issue. In this regard, this concern for environmental sustainability by the banks has given rise to concept of Green Banking. In an emerging economy like India, environmental management needs to be the key focus area of the business fraternity and especially the banking industry being the major intermediary. This would help the firms in the emerging economies utilize their limited resources in an optimum way without harming the natural environment and face the global challenge of sustainability in successful manner. In the present paper green banking and sustainability has been discussed in detail. The paper also highlights on the stages, initiatives, benefits and future of green banking in Indian context. Some case studies in Indian context are also being discussed here in order to understand the importance of green banking in the present times. The paper also discusses about the various organizations and laws and guidelines for environmental conservation and sustainability and Green Banking.

Copy the following to cite this article:

Tara K, Singh S, Kumar R. Green Banking for Environmental Management: A Paradigm Shift. Curr World Environ 2015;10(3) DOI:http://dx.doi.org/10.12944/CWE.10.3.36

Copy the following to cite this URL:

Tara K, Singh S, Kumar R. Green Banking for Environmental Management: A Paradigm Shift. Curr World Environ 2015;10(3). Available from: http://www.cwejournal.org/?p=12902

Download article (pdf)

Citation Manager

Publish History

Introduction

Banks can play a crucial role in maintaining sustainability by becoming a promoter of sustainability. Sustainable development tends to shift the focus of the business fraternity from their traditional bottom line approach of profit to the approach of triple bottom line where the focus lies on three Ps i.e. People (society), Planet (environment) and Profit (economy) and the decision point is the point of intersection of the three considerations (Fig. 1).

|

Figure 1: The Triple Bottom Line Approach Click here to View figure |

Banks and all the financial institutions are focusing on the environmental protection with the purpose of fulfilling the dual role. The first role is to work towards ethically and socially responsible banking and second as an important role of their corporate social responsibility. Banks have realized the importance of triple bottom line in their day to day functioning and so its main motive of profit has now shifted towards three Ps. And this theme has worked as a drive towards ‘Green Banking’ concept.

The present paper explores and examines green banking and sustainability, sites examples of two Indian Banks, the first one is the largest public sector bank in India i.e. The State Bank of India and the second bank is the largest private sector bank in India i.e. the ICICI bank as case studies. These banks have pioneered the green banking practically and are setting up an example for others to follow and save the degrading environment. It has been understood from the extensive literature survey and personal visit to the banks that not much has been done in this regard in India although the role of the financial institutions and especially the banks is very crucial in India’s emerging economy.

Objectives

The study mainly aims at understanding the green banking philosophy adoption by the banks. The paper attempts to review various guidelines for environmental conservation and sustainability along with the initiatives taken by the State Bank of India and the ICICI Bank.

Research Methodology

The study mainly includes literature review from secondary data. The secondary data sources include reports of the respective banks and other relative information published on the banks and other internet sites. The study also includes the primary data collection through personal visit to the bank and in-depth interviews of the branch managers.

Green Banking: Definition

Though green banking (environment-friendly banking, ethical banking or sustainable banking) can be defined in a number of ways, in a broader perspective, it is the environment-friendly banking practices that promote their customers to reduce the carbon footprint through their banking activities. The Indian Banks Association defines it as “Green Bank functions like a normal bank along with considering the social and environmental factors for the protection of the natural resources”. According to RBI (IDRBT, 2013), green banking is to make internal bank processes, physical infrastructure and Information Technology effective towards environment by reducing its negative impact on the environment to the minimum level. The UNEP-FI (2007) states that sustainable bank considers the impacts of its operations, various products and services for the current as well as future generation. In order to promote reduction in the external carbon emission, the banks should focus on financing the technology and projects that are environment friendly. Green banking aims at improving the operations and technology along with making the clients habits environment friendly in the banking business. It is like normal banking along with consideration for the social as well as environmental factors for protecting the environment. It is the way of conducting the banking business along with considering the social and environmental impacts of its activities (Jha and Bhoome, 2013; Mishra, 2013; Biswas, 2011). There are other definitions for green banking concept but the central meaning is the same i.e. protecting the environment and resources for future generation by looking for sustainable development. It includes various activities in banks’ day to day activity. Green banking includes several products and services like green mortgage, green loans, green credit cards, green savings accounts, green checking accounts, green money markets accounts, mobile banking, online banking, etc. Green Bank provides effective market based solution for addressing a wide range of environmental problems like climate change, deforestation, issues related to air quality and loss of biodiversity. Besides this, it also aims at identifying and creating various opportunities for the benefit of the customers. According to Rashid (2010), banks should prioritize in providing loans to the sectors that promote various environmental protection activities. Mani (2011) states that banks act as corporate citizens that are socially responsible in their activities. The bank set up with the purpose of sustainable banking is Triodos Bank, Netherlands. This bank is also pioneer in launching of “Green Fund” for financing green projects (Dash, 2008) and finances only those organizations which work on social, cultural and environmental values.

Sustainable Development and Sustainable Banking

According to the “report of the World Commission on Environment and Development Sustainable Development” (United Nations, 1987), Sustainable Development is the way of using the resources that not only meet the human needs of present and future generation but also preserve the environment. The field of sustainable development comprises of three constituents - environmental sustainability, economic sustainability and socio-economic sustainability. Sustainable banking as per the United Nations Environment Programme Finance Initiative (UNEP-FI, 2007) is defined as “the process by which the banks consider the impact of their various operational activities and their products and services for meeting the needs of the current as well as the future generations”.

Banking sector is under huge pressure from its different shareholders to carry out its business in ethical ways (Frenz, 2005; Jeucken, 2001). Many initiatives have been taken to promote sustainable banking across the globe and one very important such initiative is establishment of United Nations Environment Programme Finance Initiatives (UNEP-FI) in 1990. Few countries have imposed heavy penalties to banks for violating socio-economic principles e.g. the US Comprehensive Environmental Response Compensation and Liability Act (CERCLA) lead to loss to the banks in the United States. The penalty was imposed to many banks in the United States for pollution of the environment by the clients whom the banks had financed. Those banks were made to pay huge remediation cost.

The UNEP-FI (2007) states that sustainable banks consider the effects of its services and operations in meeting the needs of current as well as future generation. Direct impacts of banks are related to its products and services. (UNEP FI, 2007). Sustainability in banking sector has basically two forms (Lalon, 2015). Firstly, through adoption of environmental and social responsibility in bank’s day to day operations like wise use of paper, energy conservation etc. and secondly, by including sustainability in to banks’ products and strategies like green lending, etc.

Environmental Management by the Bank

Banks play major role in the country’s economy and in the sustainable development. Bank being the major financer indirectly contributes to the environmental degradation by financing the projects and the industries whose activities put negative impact to the environment. Thus, the bank by their active participation in the lending business in a judicious manner can contribute greatly to the environment and to the society. Banks are now adopting various strategies where the projects are scrutinized using a set of tools that take environmental considerations. Banks are also encouraging projects that show its concern for the environment in the form of sustainable development, use of renewable natural resources, waste minimization, pollution prevention, occupational health and safety, energy efficient, care of human health and many similar attributes that tries for the betterment of the society

The bank should also see that their clients comply with the environmental norms while operating their projects and conduct a regular reporting on various environmental criteria. The government should see that there is legislation that can force banks to adopt environmental policy statements and also make the customers aware of it.

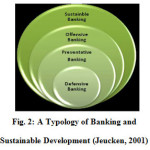

Stages of Sustainable Banking

Marcel Jeucken in his book “Sustainable Finance and Banking” (2001) has mentioned four phases action, that banks should adopt for sustainability. These stages include defensive banking, preventive banking, Offensive banking and Sustainable Banking.

As depicted in Fig. 2 below, this model consists of the four phases which have been mentioned above. Each outer layer contains the previous layer expect of the first layer i.e. the defensive banking. According to Bouma et al. (2001), every bank normally follow these stages but the attainment of sustainable approach is the most difficult one for the banks. The banks continue to evolve according to the stakeholder expectation. Here the terms ‘defensive’, ‘preventative’ and ‘offensive’ are defined in context of environmental issues.

|

|

Defensive Banking

In this phase, banks are not active and resist the environmental legislations as it affects the banks’ interest. Consideration of the environmental issues at this stage is an avoidable cost.

Preventative Banking

Due to various driving forces like government pressure, non-government organizations, pressure from society etc, banks integrate the environmental issues and risk management activities in to their daily business activities (Bouma et al, 2001)

Offensive Banking

In this stage, the banks not only consider their internal activities but also consider their external activities. The banks in this stage develop and market environmental-friendly projects. For example Green financing i.e. investing in to environmental friendly projects. The focus is on financing various projects which work on renewable energy, investment funds that invest on environment friendly assets and release of various reports based on the environmental performance.

Sustainable Banking

At this stage all the activities of banks are sustainable. Banks do not invest in the ecologically unsound business despite huge profit. The banks do not aim towards highest financial rate of return. The key motive is to get the highest sustainable rate of return. Currently, sustainable banking is possible only for the niche players of the field. Few example for this are- Triodos Bank in Netherlands and Co-operative bank in the UK.

Environmental Impacts of the Banks

Although banks do not appear to have any direct impacts on the environment, it is not so. Banks play a very crucial role in the society and as a financer to major developmental projects their role in the society and impacts on the environment cannot be neglected. Following are the major types of the environmental impacts of the banks.

Internal Impacts

Banking sector is considered as a clean sector which is technologically strong with minimum negative impact on the environment and the society. Direct impacts of the banks are related to the internal operations of the banks that may increase greenhouse emissions, like energy consumption from lights, use of computers and ATM machines, water, waste disposal, business travels etc. The direct impact of banks’ energy, waste and paper use on the environment is comparatively less than many other sectors but since the size of the banking sector is large, their impact on the environment as a whole sector cannot be ignored.

External Impacts

It is related to the environmental impacts of banks’ products and clients’ performance. But the situation is that opposite compared to other sectors in the economy. The banks’ products are not environmentally unsafe but the clients of the bank who use those products put negative impact on the environment. So it is not easy to estimate the environmental impact of banks’ external activities as the banks themselves do not have negative environmental impact rather the users of these products put negative impact on the environment.

The Environmental Risks for Banks

Banks are exposed to many risks that may lead the banks face loss in terms of reputation and profit. Banks may not get their money back which they have used to finance their clients and so can face credit risk and reputational risks. So, the risk to the banks from banks’ commercial lending activity is high. Thus, besides the liability from the banks’ own operations, greater risks are from bank’s commercial lending and can be categorized into following types (Weber et al., 2005; Weiler et al., 1997)

Risk of Loan Default by Debtors

If the loan debtors violate the environmental legislations, then they have to pay extra cost as a cost of for cleanup. This extra burden of payment many times leads bank clients become financially weak and this makes them defaulter of repaying the loan to the bank.

Risk of Reduced Value of Collateral

If the property which the bank has accepted as collateral, gets polluted, then its value detoriates due to the cost which is paid as cleanup cost. This risk increases the risk of the repayment of the expected amount.

Risk of Changing Market with Environmental Concerns

Due to increase in the environmental concern among the customers and release of strict environmental regulations, the survival of the organization without environmental concern is becoming very tough in the present times. Thus, the change in the attitudes towards the environment can make the debtors tough to survive by affecting the banks capability to repay the loan amount to the bank.

Risk of Bank’s Liability

As banks may have direct business with the collateralized properties, banks become liable for the cleanup of contamination caused by the property.

Risk of Reputation Damaged

If the banks do not perform their environmental and social responsibilities then this lowers the credibility of the bank among the public and thus causing loss of reputation of the bank.

Organizations Promoting Sustainability Concept and Green Banking

International Finance Corporation (IFC):

The IFC is a member of the World Bank Group. It finances various private sector investments and provides advisory services to various business and government. It promotes the sustainable growth of the economy. It finances various private sector investment and provides advisory services to various business and government. It promotes sustainable growth of the economy through various activities like generation of tax revenues, job creation, improving corporate governance and environmental performance. (IFC: World Bank).

United Nations Environment Programme - Financial Initiatives (UNEP-FI)

UNEP was established in the year 1972. It promotes environment protection and facilitates the wise use of the natural environment for the promotion of the sustainable development across the globe. UNEP through its initiatives works with the financial institutions towards encouraging the sustainability issue in the corporates’ financial decisions. UNEP FI is a global partnership between UNEP and the financial sector. Over 200 institutions, including banks, insurers and fund managers, work with UNEP to understand the impacts of environmental and social considerations on financial performance (UNEP FI, 2007).

Bank Track

The prime focus is towards the working of the private banks and the project they are involved in context to the environment, society and human rights. Bank Track releases research reports focused on sustainability in the banking sector. The main purpose is to promote changes in the operations of the bank so that the banks consider the ecological well being of the society and be accountable for the activities of their shareholders (Bank Track: Wikipedia).

Laws and Guidelines for Environmental Conservation and Sustainability

Equator Principles

These are the framework for the risk management. These frameworks are being adopted by various financial institutions including the banks. these framework aim at managing various environmental and social risks in the projects. The various services to which the equator principle is applicable are Project Finance Advisory Services, Project Finance, Project-Related Corporate Loans and Bridge Loans. Currently, 80 Financial Institutions have adopted the equator principle which covers 70% of the international Project Finance debt in the emerging market. (About the Equator Principles).

The Carbon Disclosure Project

The Carbon Disclosure Project (CDP) is an organization based in the United Kingdom which works with shareholders and corporations to disclose the greenhouse gas emissions of major corporations. It conducts the climate change programme for the reduction of greenhouse gas emission in order to reduce the climate change risk. CDP maintains the largest database on the climate change. It is an independent non-profit organization. Various Indian financial institutions which are signatory to the CDP are SBI, HDFC Bank Ltd, IDBI, IDFC, Reliance Capital, Tata Capital, IndusInd Bank and Yes Bank. (Business Standard, 2011).

CERCLA

Comprehensive Environmental Response, Compensation, and Liability Act of 1980 (CERCLA) is a United States federal law designed to clean up sites contaminated with hazardous substances as well as broadly define "pollutants or contaminants”. Under CERCLA, Environmental Protection Agency (EPA) can require liable parties to conduct cleanups or EPA can conduct a cleanup and subsequently seek cleanup costs from liable parties. Under CERCLA many banks in United States had to face loss when they were found responsible for the pollution activities performed by their clients.

BSE Greenex

Bombay Stock Exchange has launched its carbon-efficient equity index called ‘BSE-GREENEX’ which measures the performance of the companies in context to their Carbon Emissions (Shree, 2012). This is the second thematic index launched by BSE and this index has been launched in collaboration with IIM Ahmadabad. The index will target those investors who are socially-aware and concerned with the environment and are also willing to pay a premium for green investments in companies to get better return. The BSE Greenex will assess the energy efficiency of firms, based on energy and financial data. The selection of companies was on the basis of greenhouse emissions in the last four financial years from 2007-08 till 2010-11(Gupta, 2012).

Green Banking Industry in India

Green banking requires a fundamental change in the planning process of the banks with the adequate consideration about the economy, business, finance, society and also the banks’ profit. This will also help in the ecological balance. If we see the green banking concern in Indian banks then we will find that they are far behind the global trends. None of the Indian banks have adopted Equator Principle despite the RBI instructions. Also, none of the Indian banks are signatory to the UNEP-FI. But in recent few years, various Indian banks have started working towards this goal and have adopted various important contributions.

State Bank of India in partnership with the Suzlon energy has set up their wind mills to generate power in three states of India i.e. Gujarat, Tamil Nadu and Maharashtra for their own consumption. The State Bank of India has also started Green Channel counter (GCC) to initiate various paperless transaction activity of the banks in the branches like cash deposit, cash withdrawal and fund transfer up to Rs 40,000. Indus Ind bank has set up Solar power ATM to save 1980 KW of energy per hour every year to reduce carbon emissions. Yes Bank under community development initiatives, called “Planet Earth” is promoting clean and green drives energy efficient practices and local disaster management plans at its retail branches. ICICI Group Companies have saved around 30,000 trees and 16 crore litres of water through their various environmental friendly activities. The bank has also supported other organizations to adopt green philosophy by providing them fund to manage environment-friendly technology projects.

Bank investing or lending to those businesses and projects which have environment-friendly approach can set a trend for the companies in order to survive in the environmentally friendly market.

Green Initiatives: Indian Banks Case Studies

Case Study I: State Bank of India

SBI is the largest public sector bank in India in terms of market capitalization, profit, net profit, revenue and assets. Till December 2013, SBI had maintained assets worth US$388 billion. The bank had 17,000 branches across the globe, which also includes 190 foreign offices. This makes SBI, the largest banking and financial services company in India in terms of asset. The bank offers various ranges of activities such as commercial banking, investment banking, consumer banking, assets management, pension, credit card, insurance and mortgages. The bank was ranked 29th in Forbes 2009 ranking. It is involved in community service activity since 1973 and sponsors various social and welfare activities. State Bank has been undertaking several environmentally and socially sustainable initiatives across the country and is one of the few banks in the country to have enunciated a Green Banking Policy, since 2007.

Certain major initiatives of SBI (Mishra, 2013; Singh and Singh, 2013) are:

- With the aim of reduction of carbon footprint, SBI has collaborated with Suzlon Energy Limited for using wind power at the place of thermal power in three states namely, Gujarat, Maharashtra, and Tamil Nadu in the year 2010, (Economic Times, 2010).

- In 2010, SBI started the facility of Green Channel Counter and made it available at more than 5000 branches across the country till 2011. It is an approach towards paperless banking. This process is environmentally friendly as it consumes no paper.

- SBI supports environmentally friendly residential projects and provides concessions on loans for the projects which are rated by the Indian Green Building Council (IGBC).

- SBI provides project loans on concessional rates for the purpose of reducing green house gas emission by adoption of clean technology.

- State Bank of India has become a signatory investor to the Carbon Disclosure Project (CDP), a collaboration of over 550 institutional investors with assets under management of USD 71 trillion.

Case Study II: ICICI Bank

ICICI Bank is the second largest bank (including both private and public sectors) in India by assets and revenue whereas largest bank in the private sector. It offers various banking products and financial services such as corporate and retail banking, investment banking, assets management, insurance, venture capitalist. Currently, this bank has a widespread network of 81,254 employees and 3350 branches across the country. The bank also operates in 18 other countries across the globe. The bank is actively engaged in various social and welfare activities helping in achieving some remarkable contributions in the fields of social, environmental and economic welfare with the help of ICICI Foundations. Following are some of the important contributions of ICICI Bank in the area of green banking (D’Monte, 2010; Mishra, 2013; Singh and Singh, 2013):

- The bank provides 50 % waiver on the processing fee of car models which are using alternate modes of energy such as LPG (Liquefied Petroleum Gas) and CNG (Compressed Natural Gas). For this purpose they have identified maruti’s LPG version of Maruti 800, Omni, Hyundai’s Santro Eco, Reva Electric Car, Tata Indica CNG and Mahindra Logan CNG Version.

- Provided assistance in various activities that helped in widespread of the ISO: 14000, which is an Environmental Management System Certification.

- ICICI bank along with other organizations is working on Green Business Centre an initiative taken to promote green building, energy efficiency, recycling etc.

- ICICI bank has associated with Indian Government and the World Bank for financing SMEs for green research initiatives.

- The bank has associated with Indian Army for various water management and energy conservation initiatives.

Major benefits of Green Banking identified from in-depth interviews of the Bank Employees

In India, green banking is in its initial phase. Banks can utilize green banking as an opportunity to gain advantage in the market by creating a difference in their strategy making process. Also, banks need to be more active in communicating the green banking concept and its associated benefits to the consumers. It was also observed that green banking consciousness is high in the higher levels of management in the banks and this consciousness reduces with the lower levels of management and least with the employees who are in day to day direct touch with the customers. Thus, the banks must focus on promoting the consciousness and benefits of the green banking to the employees who are in direct touch with the customers.

Green banking is a pro-active way of energy conservation and environment protection. The prime benefit of the green banking approach is the protection of the natural resources and the environment. Green banking avoids paper work to the optimum level and focuses on electronic transactions like use of ATM, mobile banking, online banking etc for various banking transactions by the customers. Electronic transaction not only aids towards sustainability but also provides convenience to the customers as well as to the banks. Less paperwork means less cutting of trees. For implementing eco friendly business, banks should adopt environmental standards of lending as it improves the asset quality of the banks. This activity of the bank also has a very significant influence on the environmental performance of its clients. This forces the clients to perform in an environment friendly way. This not only enhances the reputation of the bank but also helps them face the environmental regulations in successful way and thus leading to better legal risk management by the banks. The banks normally grant loan to the clients on a low rate of interest. This promotes more and more entrepreneurs to start with environment friendly projects and thus leads to more and more awareness on the environment protection activities in the economy as a whole. It is thus a win-win approach by the banks as it not only benefits the environment but also the banks and its customers as a whole. Some of the major benefits of green banking to the banks identified from the interviews of the managers are as follows:

Reduces the Transaction Cost of the Bank

Green banking avoids paper work to the optimum level and follows electronic media for various transactions, banks functioning and customer management. Like providing e-statements to the customers, opening of the accounts through online, making all the internal circulars within the banks online, etc. Thus, Paperless banking reduces the transaction cost.

Competitive Edge

It helps the banks to get a competitive edge over their competitors through innovation in their products and services.

Better Risk Management

It provides the benefit of better risk management to the banks. Better risk management helps in building good image of the banks and by thus reducing the reputational risk.

Reduces the Credit Risk

It helps easy recovery of the financed loan and thus reduces the credit risk of the bank.

Cost Conscious Process

The transaction cost incurred to the bank through green banking products like ATM, Mobile banking and online banking is very less compared to the cost incurred through customer visiting the branch and performing the transaction.

Convenient Process

Green Banking provides convenience to the bank and also to the bank customers. Due to various green banking initiatives like ATM, online banking, mobile banking etc, the foot fall of the customer reduces to a larger extent in the branches of the banks and this leads to reduced cost and effort in the management of the banks activity. These banking activities also provide convenience to the consumers in terms of time management, energy and fuel conservation as they need not visit the branch for every transaction.

Future of Green Banking

Indian economy is an emerging economy and there is a huge potential of growth of Indian banks by adoption of innovative approach in their strategy making process. There is a need of an approach towards paradigm shift by setting up of the business model which would consider all the three aspect of triple bottom line approach i.e. the people, the planet and the profit. The future of green banking seems to be very promising in India as lots of green products and services are expected in the future. Green excellence awards and recognitions, Green rating agencies, Green investment funds, Green insurance and Green accounting and disclosure are some of the things that would be heard and seen in operation in the near future. Proper green banking implementation will act as a check to the polluting industries. Banks can act like a guideline towards the economic transformation and create a platform that would create many opportunities for financing and investment policy and contribute towards creation of a low carbon economy.

Conclusion

Green banking refers to the initiatives taken by the banks to encourage environment-friendly investment. Green banking as a concept is a proactive and smart way of thinking towards future sustainability. In the emerging economies, it is very important for the banks to be pro-active and accelerate the rate of the growth of the economy. As there is a continuous change in the environmental factors leading the banks face intense competition in the global market, the banks need to adhere to the stringent public policies and strict law suits. Banks need to apply morality of sustainability and responsibility to their business model, strategy formulation for products and services, operations and their financing activities and become stronger. By adopting the environmental factors in their lending activities, banks can recover the return from their investments and make the polluting industries become environment-friendly.

Adoption of green approach is more than just becoming environment-friendly as it is associated with lots of benefits like reduction in the risk as well as the cost of the bank, enhancement of banks reputations and contribution to the common good of environmental besides enhancing the reputation of the bank. In a broad sense, green banking serves the commercial objective of the bank as well as the corporate social responsibility. Thus, it is important that Indian Banks should realize their responsibilities towards the environment as well as the society in order to compete and survive in the global market.

References

- Arrowsmith D.K., Place C.M. An Introduction to Dynamical Systems, Cambridge University Press. 1994.

- Dekemele., Kevin., Robin De Keyser., Mia Loccufier. Performance measures for targeted energy transfer and resonance capture cascading in nonlinear energy sinks. Nonlinear Dynamics. 2018;1-26.

- Farid, Maor, and Oleg V. Gendelman. Tuned pendulum as nonlinear energy sink for broad energy range. Journal of Vibration and Control. 2017;23(3):373-388.

- Gendelman O. V., Manevitch L. I., Vakakis A. F. M’Closkey R., Energy Pumping in Nonlinear Mechanical Oscillators: Part I- Dynamics of the Underlying Hamiltonian Systems, J. Appl. Mech. 2001;68:34-41.

- Gendelman O. V. Bifurcations of nonlinear normal modes of linear oscillator with strongly nonlinear damped attachment, Nonlinear Dynamics. 2004;37:115-128.

- Hansen V. L., Gray J. eds. History of Mathematics. EOLSS Publications. 2010.

- Jones C.K.R.T. Geometric Singular Perturbation Theory, Dynamical Systems, Lecture Notes in Mathematics, Springer Verlag. 1995.

- Karagiannis I., Theodossiades S., Targeted energy transfer in hypoid gears of automotive differentials, ENOC. 2011.

- Maaita J.O., Meletlidou E., Vakakis A.F., Rothos V. The effect of Slow Flow Dynamics on the Oscillations of a singular damped system with an essentially nonlinear attachment, Journal of Applied Nonlinear Dynamics. 2013;2(4):315-328.

- Maaita J.O., Meletlidou E., Vakakis A. F., Rothos V. The dynamics of the slow flow of a singular damped nonlinear system and its Parametric Study, Journal of Applied Nonlinear Dynamics. 2014;3(1):37–49.

- Maaita J.O., Meletlidou E. The Effect of Slow Invariant Manifold and Slow Flow Dynamics on the Energy Transfer and Dissipation of a Singular Damped System with an Essential Nonlinear Attachment, Journal of Nonlinear Dynamics Volume 2014, Article ID 208171, 10 pages. 2014.

- Maaita J.O. Theorem on the Bifurcations of the Slow Invariant Manifold of a System of Two Linear Oscillators Coupled to a k-order Nonlinear Oscillator, Journal of Applied Nonlinear Dynamics. 2016;5(2):193–197.

- L. I. Manevitch. Complex representation of dynamics of coupled oscillators, in Mathematical Models of Nonlinear Excitations, Transfer Dynamics and Control in Condensed Systems, Kluwer Academic Publishers/Plenum, New York. 1999;269-300.

- Motato., Eliot., Ahmed Haris., Stephanos Theodossiades., Mahdi Mohammadpour., Homer Rahnejat., P. Kelly., A. F. Vakakis., D. M. McFarland., L. A. Bergman. Targeted energy transfer and modal energy redistribution in automotive drivetrains. Nonlinear Dynamics. 2017;87(1):169-190.

- McFarland D. M., Bergman L. A, Vakakis A. F. Experimental study of non-linear energy pumping occurring at a single fast frequency, Int. J. Nonlinear Mech. 2005;40:891-899.

- Nucera F., Lo Iacono F., McFarland D. M., L. A. Bergman L.A., Vakakis A. F. Application of broadband nonlinear targeted energy transfers for seismic mitigation of a shear frame: Experimental results, J. of Sound and Vibration. 2008;313:57-76.

- Saeed., Adnan S., Mohammad A. AL-Shudeifat. A New Type of NES: Rotary Vibro-Impact, ASME 2017 International Design Engineering Technical Conferences and Computers and Information in Engineering Conference. American Society of Mechanical Engineers. 2017.

- Tripepi., Concetta. et al. Application of Targeted Energy Transfer (TET) Techniques to the Seismic Protection of a Small Scale Multistory Eccentric Steel Structure, ASME 2011 International Design Engineering Technical Conferences and Computers and Information in Engineering Conference. American Society of Mechanical Engineers. 2011.

- Vakakis A. F. Inducing Passive Nonlinear Energy Sinks in Vibrating Systems, J. Vib. Acoust. 2001;123:324-332.

- Vakakis A. F, Gendelman O. V. Energy Pumping in Nonlinear Mechanical Oscillators: Part II- Resonance capture, J. Appl. Mech. 2001;68:34-41.

- Vakakis A. F., Gendelman O. V., Bergman L. A., McFarland D. M., Kerschen G., Lee Y. S. Nonlinear Target Energy Transfer in Mechanical and Structural Systems, Springer Verlag. 2008.

- Viguie R., Kerschen G., Golinval J. C., McFarland D. M., Bergman L. A., Vakakis A. F., van de Wouw N. Using Targeted Energy Transfer to Stabilize Drill-string Systems, Mechanical Systems and SignalProcessing. 2009;23:148-169.

- Wiggins S. Global Bifurcations and Chaos, Analytical Methods, Applied Mathematical Sciences, Springer Verlag. 1988.